T Bills are ultra-short-term treasury bonds backed by the full faith and credit of the U.S. government. Here we'll check out the best T Bill ETFs to buy treasury bills in 2025.

Disclosure: Some of the links on this page are referral links. At no additional cost to you, if you choose to make a purchase or sign up for a service after clicking through those links, I may receive a small commission. This allows me to continue producing high-quality content on this site and pays for the occasional cup of coffee. I have first-hand experience with every product or service I recommend, and I recommend them because I genuinely believe they are useful, not because of the commission I may get. Read more here.

Contents

Video – T-Bills Explained

In this video, I explain what T-bills are, how they work, and why you might want to buy them. Keep scrolling for the list of ETFs.

What Are T Bills?

T Bills, short for treasury bills, are just ultra-short-term bonds from the U.S. government. These short bonds with maturities of less than a year are called bills.

Because they're backed by the full faith and credit of the U.S. government, they possess no liquidity risk, credit risk, or default risk inherent of corporate bonds. As such, T Bills are quite literally the “risk-free asset,” as they're called. These special, seemingly boring bonds are considered a “cash equivalent.”

T Bills Performance

At this point you might be thinking this all automatically means negligible returns from treasury bills, but you'd be wrong. Their annualized historical return from 1928 to 2020 was 3.32%. The average rate of inflation over that period was 3.02%, which means a real return (return adjusted for inflation) of 0.3%.

How Do T Bills Work?

T Bills are sold at a discount and don't pay a coupon like most bonds, so they simply return their face value at maturity. The difference between your purchase price and that face value is your “interest.”

T Bills and Inflation

Because they're able to be rolled quickly, T Bills are also a decent inflation hedge. T Bills essentially kept pace with inflation during the double-digit inflation of the 1970’s in the U.S.! T Bills are a great place to park excess cash to be used for near-future liabilities so that you don't lose that purchasing power to inflation.

T Bills vs. Stocks

This might sound crazy, but there have also been extended periods where T Bills outperformed the stock market: the 15 years from 1929 to 1943, the 17 years from 1966-82, and the 13 years from 2000-12. Any purveyor of market history will recognize these periods as being pretty abysmal for stocks.

Stocks and treasury bonds tend to be inversely correlated, meaning when stocks zig, bonds tend to zag. Specifically, treasury bonds are a “flight to safety” asset that investors flock to during stock market turmoil or uncertainty. This has indeed been happening in 2023 so far with T-bill funds seeing record inflows as cautious investors seek yield and a safe haven with recession fears looming. In January 2023, the 3-month treasury bill rate is 4.57%.

How To Buy T Bills

T Bill ETFs allow you to avoid having to buy and roll a ladder of individual bonds yourself. Now that you know why treasury bills are attractive for a variety of purposes and audiences, let's check out the best T Bill ETFs with which to buy them.

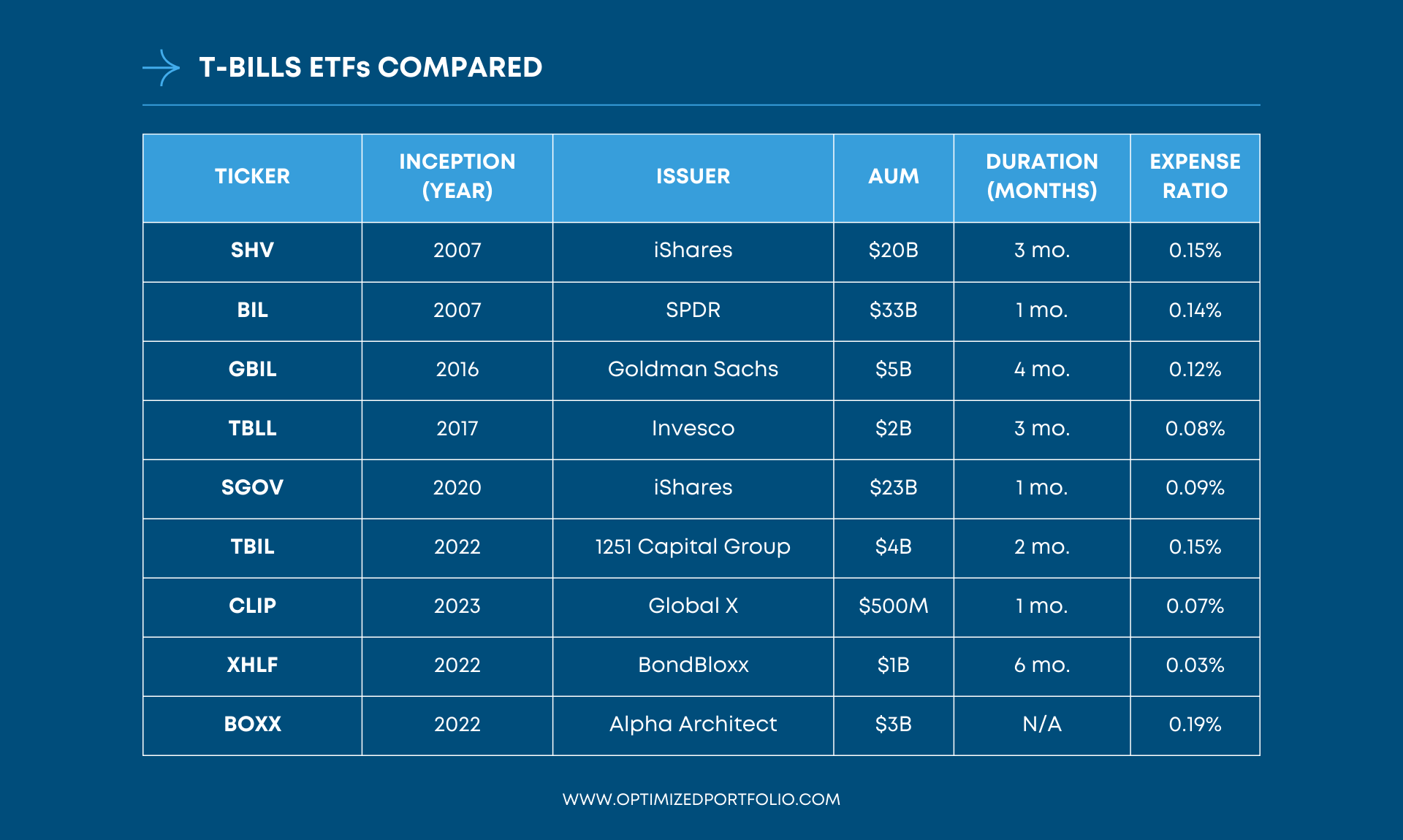

The 9 Best T Bill ETFs

Below are the 9 best treasury bill ETFs. They vary somewhat in size, effective maturity, and fees.

T Bill ETFs Video

Prefer video? Watch it here. If not, keep scrolling to keep reading.

SHV – iShares Short Treasury Bond ETF

The iShares Short Treasury Bond ETF (SHV) holds T-bills with maturities of 1 year or less. Its weighted average maturity is 4.7 months. This fund has over $20 billion in assets, likely simply because it is the oldest fund on this list. SHV has an expense ratio of 0.15% and seeks to track the Barclays Capital U.S. Short Treasury Bond Index.

BIL – SPDR Bloomberg Barclays 1-3 Month T-Bill ETF

BIL goes shorter than SHV above and holds treasury bills with maturities between 1 and 3 months. As such, BIL has comparatively less interest rate risk than SHV. Because BIL has the name recognition in this space and has been around since 2007, it has over $30 billion in assets.

BIL has an expense ratio of 0.14% and seeks to track the Bloomberg Barclays 1-3 Month U.S. Treasury Bill Index.

GBIL – Goldman Sachs Access Treasury 0-1 Year ETF

Think of GBIL as basically a cheaper version of SHV above, holding T-bills with a time to maturity of less than 1 year. The fund seeks to track the FTSE US Treasury 0-1 Year Composite Select Index and has an expense ratio of 0.12%. The fund has a little over $5 billion in assets.

TBLL – Invesco Short Term Treasury ETF

Like SHV and GBIL, TBLL from Invesco also holds T bills with less than a year left to maturity. It's newer than the other funds already discussed, with “only” about $1.7 billion in assets, but it's also cheaper with an expense ratio of 0.08%. The fund seeks to track the ICE U.S. Treasury Short Bond Index.

TBLL previously traded under the ticker CLTL and was named the Invesco Treasury Collateral ETF.

SGOV – iShares 0-3 Month Treasury Bond ETF

SGOV from iShares launched in May, 2020. It is similar to BIL, holding T-bills with maturities less than 3 months.

SGOV used to be the cheapest option on this list, but its fee waiver expired, so it now has a fee of 0.09%. Not the cheapest, but still a great option. This fund has nearly $24 billion in assets. I covered SGOV specifically in a separate post here.

TBIL – US Treasury 3 Month Bill ETF

TBIL launched in 2022 and plainly holds 3 month T-Bills, making it very similar to SGOV and BIL, though it costs more at 0.15%, which I think sort of makes it obsolete, but it has nearly $4 billion in assets. TBIL seeks to track the ICE BofA US Treasury Bill 3 Month Index.

CLIP – Global X 1-3 Month T-Bill ETF

CLIP from Global X is the newest fund on the list, having launched in mid-2023. As such, it is the least popular with only about $500 million in assets. However, it is one of the most affordable ETFs for T-Bills with an expense ratio of 0.07%.

CLIP provides plain-vanilla exposure to 1-3 month T-Bills by seeking to track the Solactive 1-3 month US T-Bill Index.

XHLF – BondBloxx Bloomberg Six Month Target Duration US Treasury ETF

XHLF is the cheapest T-Bills ETF on the list with a fee of only 0.03%. It's pretty young, having launched in late 2022, and BondBloxx is certainly not a household name, but the fund's low fee has allowed it to amass over $1 billion in assets in its short lifespan thus far.

XHLF holds treasury bills with maturities less than 1 year to aim for a target duration of 6 months, making it a bit longer than most of the other funds on this list. Appropriately, its index is the Bloomberg US Treasury 6 Month Target Duration Index.

BOXX – Alpha Architect 1-3 Month Box ETF

BOXX is the Alpha Architect 1-3 Month Box ETF. The name should hint to you that this fund aims to resemble 1-3 month T-Bills, but it's important to note right off the bat that in doing so, BOXX doesn't actually hold any T-Bills at all. It uses complex derivatives to synthetically extract a return resembling the risk-free rate of 1-3 month T-Bills, but in a much more tax-efficient manner than the other funds discussed here, because it aims to avoid distributions and to convert income to capital gains.

So while it's not a true T-Bills ETF in the purest sense, it would have been remiss to not include it on this list. BOXX has a fee of 0.19%.

Click here to read my separate post on the details of BOXX.

Recap – Comparison Chart

Here's a recap comparison chart of these ETFs for T-Bills:

Where To Buy These T Bill ETFs

All the above ETFs for treasury bills should be available at any major broker. My choice is M1 Finance. M1 has zero trade commissions and zero account fees, and offers fractional shares, dynamic rebalancing, intuitive pie visualization, and a sleek, user-friendly interface and mobile app. I wrote a comprehensive review of M1 Finance here.

Canadians can find the above ETFs on Questrade or Interactive Brokers. Investors outside North America can use Interactive Brokers.

What do you think of T-bills? Let me know in the comments.

T Bills FAQ's

Can T bills lose value?

No, T bills cannot lose value and are considered virtually riskless due to the high quality and liquidity of U.S. debt.

Can T bills be purchased in an IRA?

Yes, T bills can be purchased in an IRA.

What Treasury bill is the risk free rate?

The U.S. 3-month Treasury bill is used as the risk free rate.

How are T bills taxed?

Interest from T bills is subject to federal income taxes but not state or local taxes.

Are T bills taxable?

Interest from T bills is taxable as federal income taxes but is not subject to state or local taxes.

Are T bills a good investment?

T bills may indeed be a good investment for you if you need a safe cash equivalent investment that would be expected to generate a modest return.

Are T bills safe?

Yes, as short-term debt obligations of the U.S. Treasury, T bills are indeed safe and are considered “the risk-free asset.”

Will T bills go up?

As long as the federal funds rate (“interest rates”) is positive, T bills can only go up. At worst, they will remain flat. T bills cannot lose value.

Will T bills continue to rise?

We can't predict the future, so no one knows if the interest rate of T bills will continue to rise. Interest rates can go up or down and are basically unpredictable. T bills themselves cannot lose value, though,

Why are T bills issued?

The United States government issues T bills to fund public projects like schools and highways

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

Disclaimer: While I love diving into investing-related data and playing around with backtests, this is not financial advice, investing advice, or tax advice. The information on this website is for informational, educational, and entertainment purposes only. Investment products discussed (ETFs, mutual funds, etc.) are for illustrative purposes only. It is not a research report. It is not a recommendation to buy, sell, or otherwise transact in any of the products mentioned. I always attempt to ensure the accuracy of information presented but that accuracy cannot be guaranteed. Do your own due diligence. I mention M1 Finance a lot around here. M1 does not provide investment advice, and this is not an offer or solicitation of an offer, or advice to buy or sell any security, and you are encouraged to consult your personal investment, legal, and tax advisors. Hypothetical examples used, such as historical backtests, do not reflect any specific investments, are for illustrative purposes only, and should not be considered an offer to buy or sell any products. All investing involves risk, including the risk of losing the money you invest. Past performance does not guarantee future results. Opinions are my own and do not represent those of other parties mentioned. Read my lengthier disclaimer here.

Are you nearing or in retirement? Use my link here to get a free holistic financial plan and to take advantage of 25% exclusive savings on financial planning and wealth management services from fiduciary advisors at Retirable to manage your savings, spend smarter, and navigate key decisions.

If we buy T-Bills in ETF form (vs buying a T Bill from say TreasuryDirect), are those gains still exempt from state and local taxes? Do the tax documents we get from the brokerage firm make it clear when filing taxes, or do T-Bill ETFs complicate tax filing?

Thanks!

Yes, still exempt. Doesn’t complicate anything.

What happens if you hold BIL at the end of the month? When it rebalances are you losing money? Do you have to sell every month?

No. Interest accumulates during the month and pays out at the end, at which point share price drops. Doesn’t matter when you buy or sell. No need to sell every month.

I’m confused about how the T-Bill rate “realizes” in these funds? For example, the Jan’23 T-BIll rate ~4.5% vs. the M-1 Dividend Yield around 1.7% for SGOV or CLTL. What am I not understanding? And then, those price fluctuations in the last ~6 months… I’m trying to follow Buffet’s advice and not invest in anything I don’t understand. And I can’t just buy T-Bills in my M1 IRA, it would have to be a fund. Many thanks.

Hey Rob, looks like M1 is likely just showing the wrong yield so I can see how that would be confusing. You can go to the official iShares website to see the correct yield at any time.

Look at $boxx , apparently it uses option box spreads to match 3-month tbills in a tax efficient manner

FYI, SGOV’s fee is currently at 0.05% , and the waiver has been extended to June 30th 2023.

I’ve had a heck of a time setting up an account to purchase I-bonds. My bank and their paperwork keep hating each other. From reading your article it would appear they seem to do the same thing without the need to go through the treasury? Just a different place to get a similar inflationary hedge accomplished.

I-bonds are closer to short TIPS.

Thank you!

Do you have a personal preference? I’m looking at STIP based on your comment. 2% beats my BOA checking acct interest all day.

STIP would be fine. VTIP is comparable from Vanguard. I touched on them briefly here.